The ISM manufacturing PMI for August ticked higher from 48.0 to 48.7, just a few notches short of the 49.0 consensus to reflect another month of industry contraction. Still, the pace of decline slowed as new orders returned to growth for the first time since January.

Key Takeaways from August ISM Manufacturing PMI

- Mixed signals on demand: New orders expanded for the first time in six months (51.4% vs 47.1% prior), but production contracted sharply (47.8% vs 51.4%)

- Employment pressures persist: The employment index remained deeply in contraction at 43.8%, with companies continuing workforce reductions amid uncertainty

- Tariff impact intensifies: Prices surged to 63.7%, with steel and aluminum price increases flowing through the entire value chain

- Supply chain stress returns: Supplier deliveries slowed (51.3% vs 49.3%), potentially signaling demand-driven bottlenecks

- Export weakness continues: New export orders remained in contraction for the sixth month (47.6%), reflecting ongoing trade tensions

- Inventory dynamics improve: Raw materials inventories contracted at a slower pace, while customer inventories remained critically low

Link to U.S. ISM Manufacturing PMI (August 2025)

Despite the persistent weakness across the broader manufacturing landscape, artificial intelligence spending continued to provide support to select segments, while widespread tariff-related cost pressures dominated industry commentary.

Survey respondents across multiple industries highlighted the severe impact of tariff policies, with many companies reporting significant price increases and operational disruptions. Steel and aluminum tariffs were particularly cited as driving cost pressures throughout manufacturing supply chains.

The persistent weakness in exports suggests that retaliatory measures and global trade tensions continue to weigh on US manufacturing competitiveness, while domestic demand remains insufficient to offset these headwinds.

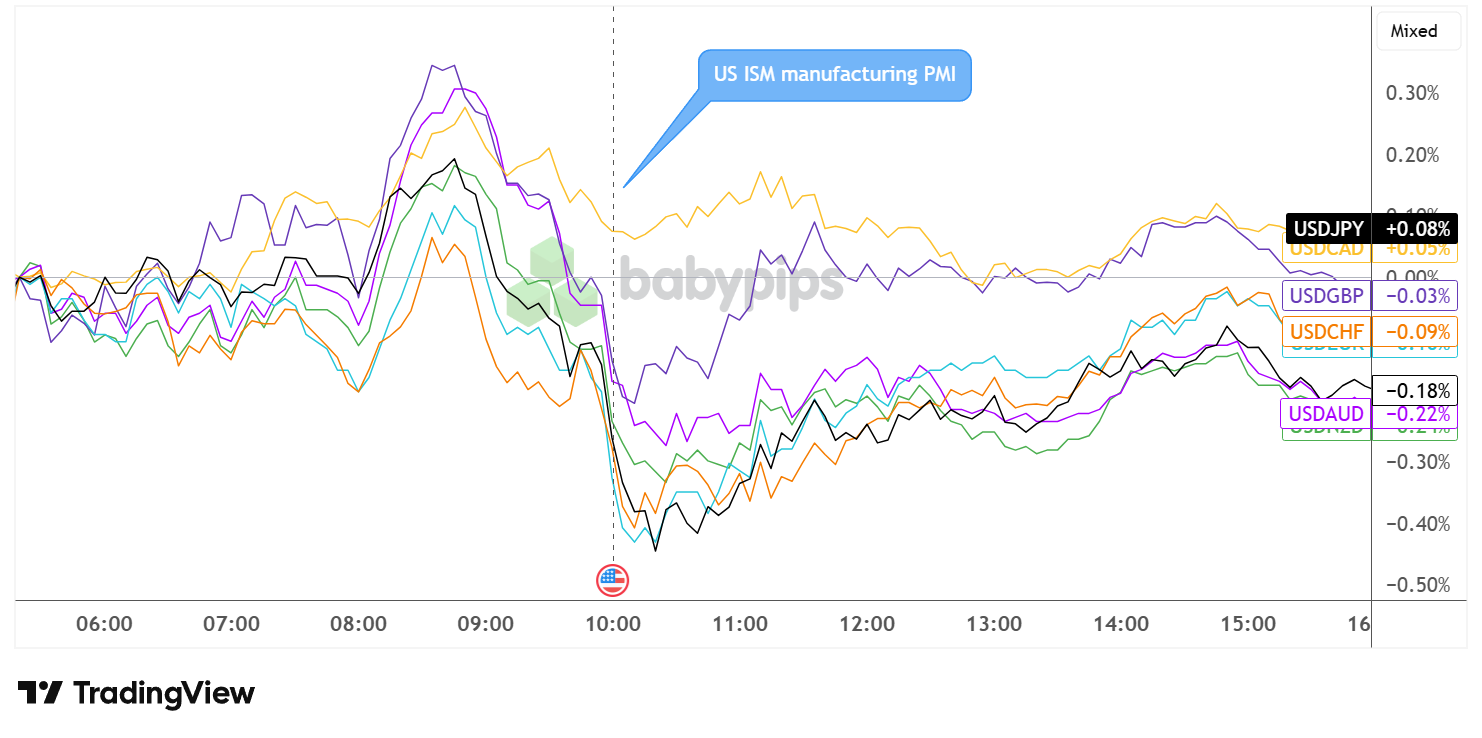

Market Reaction

United States Dollar vs. Major Currencies: 5-min

{kind=link}

Overlay of USD vs. Major Currencies Chart by TradingView

The Greenback, which had been pulling back from earlier rallies leading up to the ISM manufacturing PMI release, extended its slump after the report was printed.

However, a quick but shallow rebound soon followed as safe-haven demand appeared to be the main driver of price action for the most part of the day.

USD managed to stay afloat against the weaker CAD (+0.05%) and JPY (+0.08%) a few hours after the ISM report was released but remained in the red against AUD (-0.22%) and NZD (-0.24%).