Stay informed with free updates

Simply sign up to the Sovereign bonds myFT Digest — delivered directly to your inbox.

Last week Satori Insights’ Matt King wrote a fantastic column in the main paper on why the 30-year bond carnage that has caused such angst is actually primarily technical, rather than fundamental.

After all, if this was about inflation you’d expect it to show up in breakeven inflation rates. If it was a yuge-supply issue then surely it would also appear in other tenors of the yield curve, where countries issue more debt. And if it was really fears over sovereign creditworthiness then it makes no sense that the pain is overwhelmingly focused on the 30-year part of the curve.

That said, a lot of countries are unquestionably facing some very awkward questions when it comes to their debt burdens. A recent Goldman Sachs report has put some numbers on those concerns — and cast doubts on some of the suggested palliatives.

The main thing to remember is that even though interest rates are now falling — with the Federal Reserve expected to ease policy again later this week — it doesn’t mean that government debt servicing costs are falling as well. In fact, they’re probably going to keep rising for years to come.

A lot of countries took advantage of the low-rate era to issue more long-term bonds, lengthening the “weighted average maturity” — or WAM — of their sovereign debt stock.

That has meant that the cost of servicing their growing debt pile has remained remarkably low, despite rising rates. But eventually all those bonds sold when rates were floored and bond yields were hitting historical lows will have to be refinanced at higher costs cost in the coming years. As Goldman’s economists say:

Governments’ own forecasts generally project deficits to improve in many economies, but the long timetable for implementation, as well as the track record of slippage vs deficit projections since the pandemic, suggests persistently large deficits and elevated bond issuance will be a durable feature of the macro landscape in coming years. With market interest rate forwards well above current average interest costs, this implies further future pressure on government budgets via interest costs.

In some countries with lower WAMs — most notably the US — this has already begun to bite, but it’s going to be a growing issue almost everywhere.

Goldman Sachs looked at government deficit predictions, debt maturities and the interest rate forecasts embedded in markets, and found that Italy, the US, Japan and France are going to see the greatest increase in their debt servicing costs over the next five years.

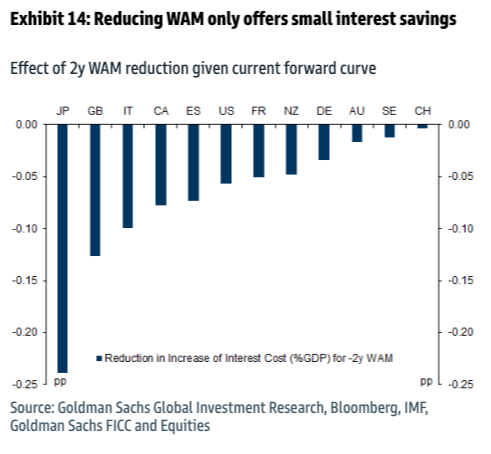

One of the solutions often offered is to issue more shorter-term bonds with lower yields.

For example, the US pays 4.6 per cent to issue 30-year bonds, but about 4 per cent for 10-year paper, and 3.5 per cent for two-year notes. For the UK the equivalent yields are 5.5 per cent, 4.6 per cent and under 4 per cent respectively. For France, it’s 4.3 per cent, 3.5 per cent and 2.1 per cent.

The “yield curve” of bond maturities isn’t particularly steep at the moment, but by selling more short-term bonds most countries might therefore be able to save some money.

Except . . . some countries have already been shortening their WAM to trim their interest rate expenses. And those that haven’t shortened the average term of their bond issuance programmes typically have such high WAMs already that it would take time for a shift in debt issuance to have any effect.

In fact, outside of Japan — which is a pretty special case — the gains that would come from a pretty hefty two year reduction in weighted average maturities is negligible (and they’re really not huge in Japan either).

Hefty central bank interest rate cuts would help more, Goldman calculates, but, well, we probably need recessions for rates to really come down aggressively, and that won’t be a good thing for tax revenues. So the investment bank’s economists instead end on a things on a funny note.

Reducing WAM by 1yr is worth 3bp. Lowering front-end rates is worth 19bp. In contrast, reducing the deficit by 1pp is worth 13bp, even without any impact on the interest rate curve — and this is an effect that would build over time given the impact on reducing the debt stock.

Absent spending cuts, wide deficits and steeper curves are here to stay. Our work suggests pressures on government budgets are unlikely to resolve quickly.

LOL. “Spending cuts.”