It is pretty unusual to launch into the world as a teenager or young adult with a strong sense of how your money works and what makes it grow. Generally this is something we all figure out along the way from parents, family and real-world experience.

But it is helpful to think about growing your money as a trade-off: if you play it safe, your money will grow slowly, but it is very likely to still be there when you want to spend it. If you take on riskier bets, you can make your money grow faster, but if you are unlucky, you can also lose it all.

Mastering Money

This article is part of Mastering Money, an FT Schools report for students and teens on how to make good financial decisions. Other articles cover social media, saving, borrowing and insurance.

For more on the FT Schools programme, which offers free FT access as well as teaching resources, click here.

Here’s our guide to some of the places you can put your money as you accumulate it, starting with the safe stuff and building up to the riskier things.

Cash: Safe. Unexciting. Not entirely risk free

To start with, there’s cash.

If you are saving up for something, gathering physical money in a safe place or putting it into a savings account at the bank is the most basic way to do it.

As long as your safe place is really safe, gathering physical notes and coins together over time does eventually build up. In your head, if you think about this cash as out of bounds, and you don’t spend it, it racks up to something bigger for you to spend later on.

The other option is to put it into a savings account at a bank. You can withdraw this cash very quickly, but if you leave it there for a while, you receive a payment called interest — like a little reward for leaving your funds there. Your interest is added to the amount you have saved and then you get paid interest on the new overall total. Shop around — you will be surprised how big the difference is in the interest rate between various providers.

The good thing about this is it’s very easy to put money in and get it out again, and it does grow over time. The bad news is that you might lose out due to inflation.

This is the process where prices generally rise gradually over time. If annual inflation in your country is 3 per cent, then the price of goods and services you buy is rising by 3 per cent a year. Ideally then, you want to receive an interest rate of at least 3 per cent, so that you can buy more with your money in future, not less. You definitely don’t get that with physical money and you may not get it with a savings account either if the interest rate is really low.

One thing you can do to get around this is lock your money away for longer — long term savings accounts generally have higher interest rates, but they may stop you from getting your hands on the money before the term is up.

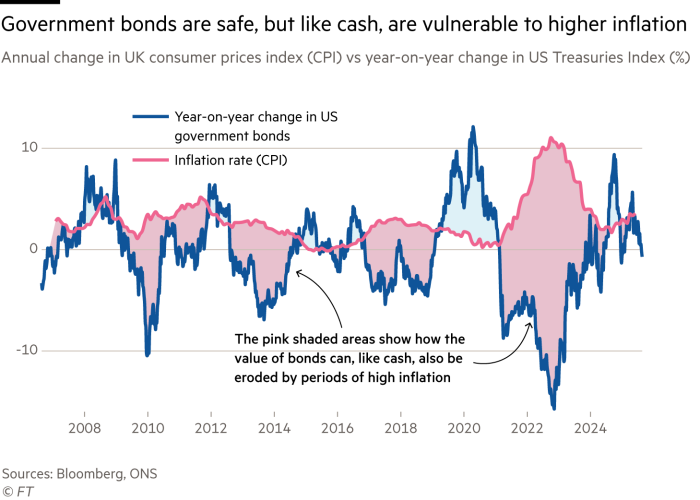

Bonds: Fairly safe. Fairly boring. A bit more complicated than a savings account

The next step up in terms of risk and reward is bonds. This is where you lend your money to the government or a company. They get money to use to pay for schools, hospitals or defence (in the case of governments) or shiny new factories (in the case of companies). In return, they promise to hand the money back after a set amount of time, and pay interest every year. The promise is called a bond.

It is tricky for individuals to invest in bonds directly, so most do it via an investment fund. Here an investment company gathers money from lots of individuals and invests in a lot of bonds. Over time, the individuals hope to see a decent increase in the amount of money they have handed over. As a rule, government bonds are very safe, so you are very unlikely to lose your money, but again, there is some risk that if inflation is running high, your money might not stretch quite so far at the end.

So, cash and bonds are the safer end of the products available. You are extremely unlikely to lose your money, but it won’t grow super fast either. Still, products based on bonds will generally be more generous than savings accounts where you don’t lock your money away for long.

Shares: You could make plenty of money. You could lose it too

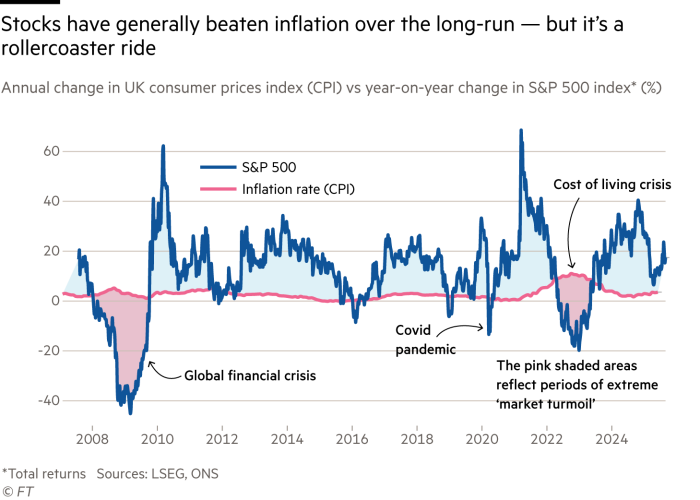

The next step up is stocks, sometimes also known as shares or equities. Imagine you take a big company, like Amazon or Apple, and you split it up into lots of little slices of ownership. You can buy a slice, a share in the company.

There are two main ways to invest in shares. Again, one is riskier than the other.

The first is to take hundreds of different companies and bundle them together into a list (called an index). Lots of companies do this bundling for you and sell funds that track how all of those companies rise or fall in value as a group. If all the companies are, as a whole, worth 10 per cent more this year than last year, then your pot of money will be worth 10 per cent more.

The beauty of this is that you spread your bets across hundreds of different companies so even if the value of some of them falls, the value of others could rise. Also, stocks in general pretty reliably beat bonds and cash for the return you get as an investor, although some years they can fall in value sharply.

If you put $100 in the US stock market back at the start of 2020, in the S&P 500 index — the world’s most important stocks index — then it would be worth $203 today.

If you want to, though, you can dial up the risk and bet on certain individual companies. If, for example, you had put that whole $100 on shares in Amazon, then that would be worth $246 today.

This is a process called stock picking, where investors choose individual stocks to buy. The danger is that sometimes companies fall heavily in value too. If you had picked Peloton instead of Amazon, then at one point your $100 would have grown to $573. Great! But now, it’s worth about $26. Not so great.

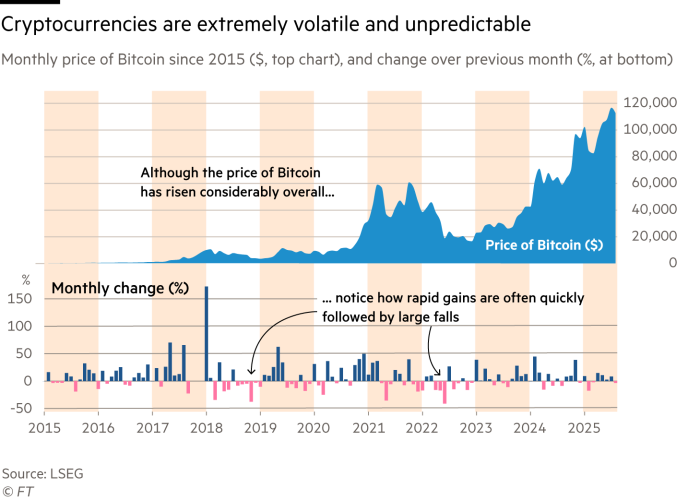

Cryptocurrency: Has made some people very rich. Has made other people very poor

This is a stupid name, really. They’re not currencies like the pound or the dollar or the euro. They are chunks of code that go up in value when more people want to own them, and down when they don’t. They are not linked to any particular company or country, and often there are limited rules to protect your money. They can make people very, very rich. One bitcoin, the biggest crypto, is worth around $115,000 now. At the start of 2020 it was worth well under $10,000.

So if you buy on the way up, you can make a lot of money. The problem with cryptos is that they can lose money quickly for no real reason too, and they often do, leaving buyers with less money than they started.

Regulators in most parts of the world are very clear about this: if you want to buy crypto, go ahead, but you must be prepared to lose all of your money and you should not expect the government to help you out in case of a disaster.