Markets kicked off the week with cautious optimism despite political turmoil in Japan and France, as risk appetite held firm on Fed rate cut expectations.

Gold hit record highs while the dollar stayed on the defensive, setting the tone ahead of Thursday’s US CPI report.

Check out the headlines and economic updates you may have missed in the latest trading sessions!

Headlines:

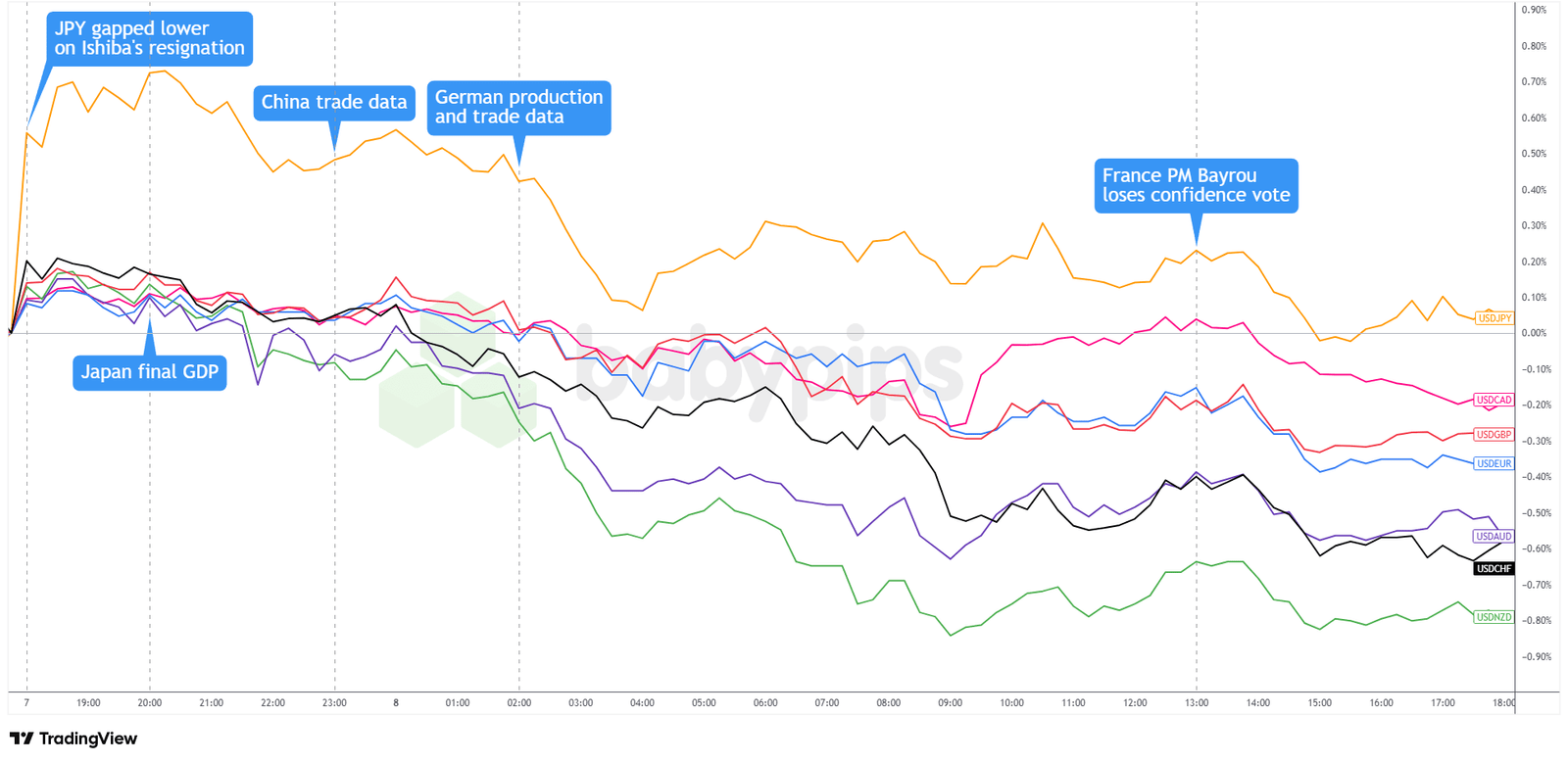

- Japanese Prime Minister Shigeru Ishiba resigned on Sunday following LDP’s election losses

-

Japan GDP Growth Rate Final for Q2 2025: 0.5% q/q (0.3% q/q forecast; 0.0% q/q previous); 2.2% y/y (1.0% y/y forecast; -0.2% y/y previous)

- Japan GDP Price Index Final for Q2 2025: 3.0% y/y (3.0% y/y forecast; 3.3% y/y previous)

- Japan GDP Capital Expenditure Final for Q2 2025: 0.6% q/q (1.3% q/q forecast; 1.1% q/q previous)

- Japan Current Account for July 2025: 2,684.0B (3,100.0B forecast; 1,348.0B previous)

- Australia Building Permits Final for July 2025: -8.2% m/m (-8.2% m/m forecast; 11.9% m/m previous)

- Australia Private House Approvals Final for July 2025: 1.1% m/m (1.1% m/m forecast; -1.9% m/m previous)

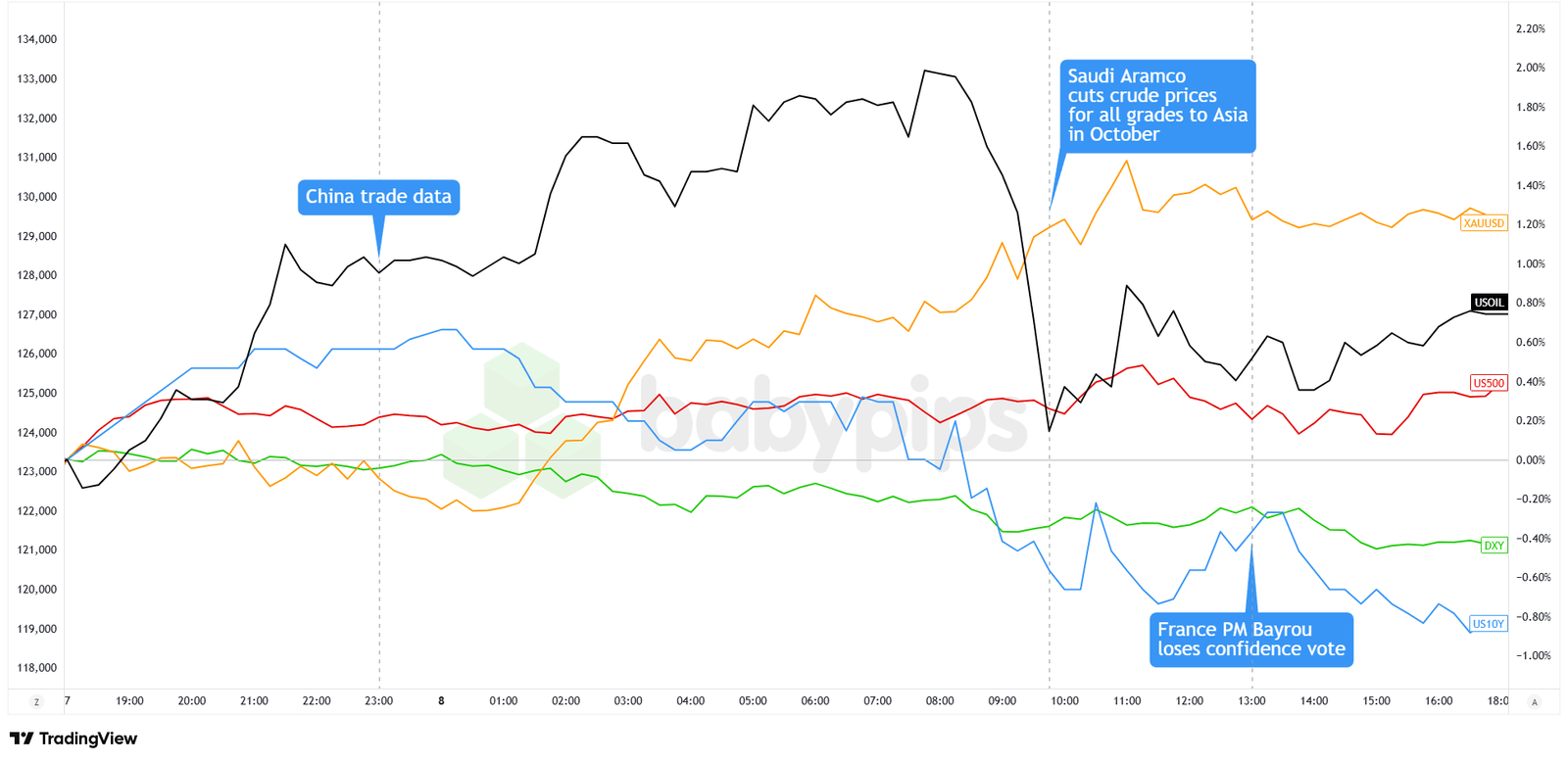

- China Balance of Trade for August 2025: 102.33B (95.0B forecast; 98.24B previous)

- Japan Eco Watchers Survey Outlook for August 2025: 47.5 (47.5 forecast; 47.3 previous)

- SNB Chairman Schlegel said they won’t hesitate to act if necessary, but the hurdle for reintroducing negative interest rates is high

- Germany Balance of Trade for July 2025: 14.7B (21.4B forecast; 14.9B previous)

- Germany Industrial Production for July 2025: 1.3% m/m (1.1% m/m forecast; -1.9% m/m previous)

- U.S. Consumer Inflation Expectations for August 2025: 3.2% (3.1% forecast; 3.1% previous)

- EU aims to coordinate with the US to sanction Russia following heaviest strikes on Ukraine

- François Bayrou ousted as French PM after losing confidence vote

- Saudi Arabia to cut oil prices for Asia as OPEC+ sticks with output hike

Broad Market Price Action:

{kind=link}

Markets started the week in cautious optimism as political upheaval rippled across major economies. European stocks posted modest gains despite French political uncertainty, with the DAX climbing 0.54% and the CAC 40 adding 0.49%, while the FTSE lagged at 0.07%. Better-than-expected German industrial production data likely provided some support.

Wall Street extended the positive momentum with the Nasdaq hitting fresh record highs, led by software stocks rallying 1.2%. The S&P 500 edged up 0.2% as traders solidified expectations for a September Fed rate cut following Friday’s disappointing employment report.

Gold surged to unprecedented territory above $3,640, driven by falling real yields as the 10-year Treasury yields dropped to 4.04%, its lowest since April. The precious metal’s relentless march higher reflected both rate cut expectations and continued central bank accumulation.

Crude oil recovered modestly to $62.40 after OPEC+ announced a smaller-than-feared production increase of 137,000 barrels per day for October, while potential Russian sanctions provided additional support. Bitcoin remained relatively subdued near $112,000, consolidating recent gains despite the broader risk-on sentiment sweeping through traditional markets.

FX Market Behavior: U.S. Dollar vs. Majors:

Overlay of USD vs. Majors Chart by TradingView

The dollar opened on a defensive footing as Asian markets digested Friday’s disappointing employment data, with traders cementing expectations for a September Fed rate cut. The yen proved the notable exception, gapping sharply lower following Prime Minister Ishiba’s weekend resignation announcement, allowing USD/JPY to briefly spike before the move was completely retraced during Tokyo trading.

The Greenback’s weakness accelerated through European hours as better-than-expected German industrial production data bolstered risk appetite, while dovish Fed bets weighed on the currency. The euro tested monthly range highs near 1.1765 as the dollar selloff gained momentum, shrugging off concerns about French political instability following PM Bayrou’s confidence vote defeat. Sterling similarly flirted with recent peaks while commodity currencies outperformed, with the Australian and New Zealand dollars posting the strongest gains among majors.

The dollar’s decline persisted after the London close as Treasury yields held near multi-month lows, with the 10-year yield anchored around 4.04%. Market participants appeared to position defensively ahead of Thursday’s crucial CPI report, which could either validate or challenge current rate cut assumptions that have the dollar trading near its weakest levels since early summer.

Upcoming Potential Catalysts on the Economic Calendar

- New Zealand Manufacturing Sales for Q2 2025 at 10:45 pm GMT

- U.K. BRC Retail Sales Monitor for August 2025 at 11:01 pm GMT

- Australia Westpac Consumer Confidence Change for September 2025 at 12:30 am GMT

- Australia NAB Business Confidence for August 2025 at 1:30 am GMT

- Japan Machine Tool Orders for August 2025 at 6:00 am GMT

- France Industrial Production for July 2025 at 6:45 am GMT

- U.S. NFIB Business Optimism Index for August 2025 at 10:00 am GMT

- Germany Bundesbank Nagel Speech at 11:30 am GMT

- U.S. Non Farm Payrolls Annual Revision at 2:00 pm GMT

- U.S. API Crude Oil Stock Change for September 5, 2025, at 8:30 pm GMT

- New Zealand Visitor Arrivals for July 2025 at 10:45 pm GMT

The London and U.S. sessions will likely stay cautious as traders hold back ahead of Thursday’s U.S. CPI, though surprises from Germany’s Nagel or U.S. jobs revisions could trigger brief swings.

Safe haven flows into the dollar and franc may continue if geopolitical tensions flare, while risk currencies could remain choppy.

As always, look out for global trade developments and geopolitical headlines that could influence overall market sentiment. Stay nimble and don’t forget to check out our Forex Correlation Calculator when taking any trades!