Risk assets had a good day on Thursday thanks to a mix of economic and earnings data, geopolitical updates, and positioning ahead of Friday’s US core PCE release.

The dollar stayed weak, while stocks, gold, and bitcoin held gains despite geopolitical jitters.

Here’s how major asset classes performed in the latest trading sessions!

Headlines:

- Russian missile and drone attack on Kyiv kills at least 19 people

- Australia private capital expenditure for Q2 2025: 0.2% q/q (0.8% forecast, -0.1% previous)

- New Zealand ANZ business confidence for August: 49.7 (49.0 forecast; 47.8 previous)

- Australia building capital expenditure for Q2: 0.2% q/q (0.4% q/q forecast; 0.9% q/q previous)

- BOJ member Nakagawa reaffirmed the central bank’s hawkish bias, but also said tariff uncertainty remains high

- Swiss GDP growth rate for Q2: 1.2% y/y (1.3% y/y forecast; 2.0% y/y previous); 0.1% q/q (0.1% q/q forecast; 0.5% q/q previous)

-

Euro Area economic sentiment for August: 95.2 (96.0 forecast; 95.8 previous)

- Euro Area services sentiment for August: 3.6 (4.5 forecast; 4.1 previous)

- Euro Area consumer inflation expectations for August: 25.9 (29.0 forecast; 25.1 previous)

- Euro Area consumer confidence for August: -15.5 (-15.5 forecast; -14.7 previous)

- Euro Area industrial sentiment for August: -10.3 (-9.0 forecast; -10.4 previous)

- ECB August meeting minutes: Maintaining policy rates at their current levels would allow more time to see how trade negotiations unfold

- German Chancellor Merz said a meeting between Ukrainian President Zelenskiy and Russia’s President Putin “won’t happen”

- Canada current account for Q2: -21.2B (-15.0B forecast; -2.1B previous)

- FOMC member Lisa Cook asked a U.S. District Judge to issue a temporary restraining order barring Trump’s firing

- U.S. initial jobless claims for August 23: 229.0k (237.0k forecast; 235.0k previous)

- U.S. GDP growth rate 2nd est for Q2: 3.3% q/q (3.0% q/q forecast; -0.5% q/q previous)

- U.S. GDP price index 2nd est for Q2: 2.0% q/q (2.0% q/q forecast; 3.8% q/q previous)

- U.S. pending home sales for July: -0.4% m/m (-0.2% m/m forecast; -0.8% m/m previous); 0.7% y/y (0.4% y/y forecast; -2.8% y/y previous)

- U.S. EIA natural gas stocks change for August 22: 18.0Bcf (13.0Bcf previous)

- U.S. Kansas Fed manufacturing index for August: 0.0 (-4.0 forecast; -3.0 previous)

- UK, France, Germany trigger UN sanctions on Iran over ‘significant’ nuclear program defiance

- EU proposed removing duties on imported U.S. industrial goods in return for reduced U.S. tariffs on European cars

Broad Market Price Action:

{kind=link}

Traders navigated a mix of corporate earnings, economic data, and political uncertainty on Thursday as traders positioned ahead of Friday’s key inflation report.

Wall Street reached new highs despite initial Nvidia-related jitters, with the S&P 500 climbing 0.3% and the Dow adding 0.2%. The Nasdaq rose 0.5% as investors viewed Nvidia’s 56% revenue surge as confirmation of sustained AI infrastructure spending, even though the company excluded potential China sales from guidance amid trade uncertainties.

European markets closed mixed, with the pan-European Stoxx 600 slipping 0.2%, the UK’s FTSE 100 down 0.4% and Germany’s DAX essentially flat, while France’s CAC 40 gained 0.2% as investors digested tech earnings and economic data.

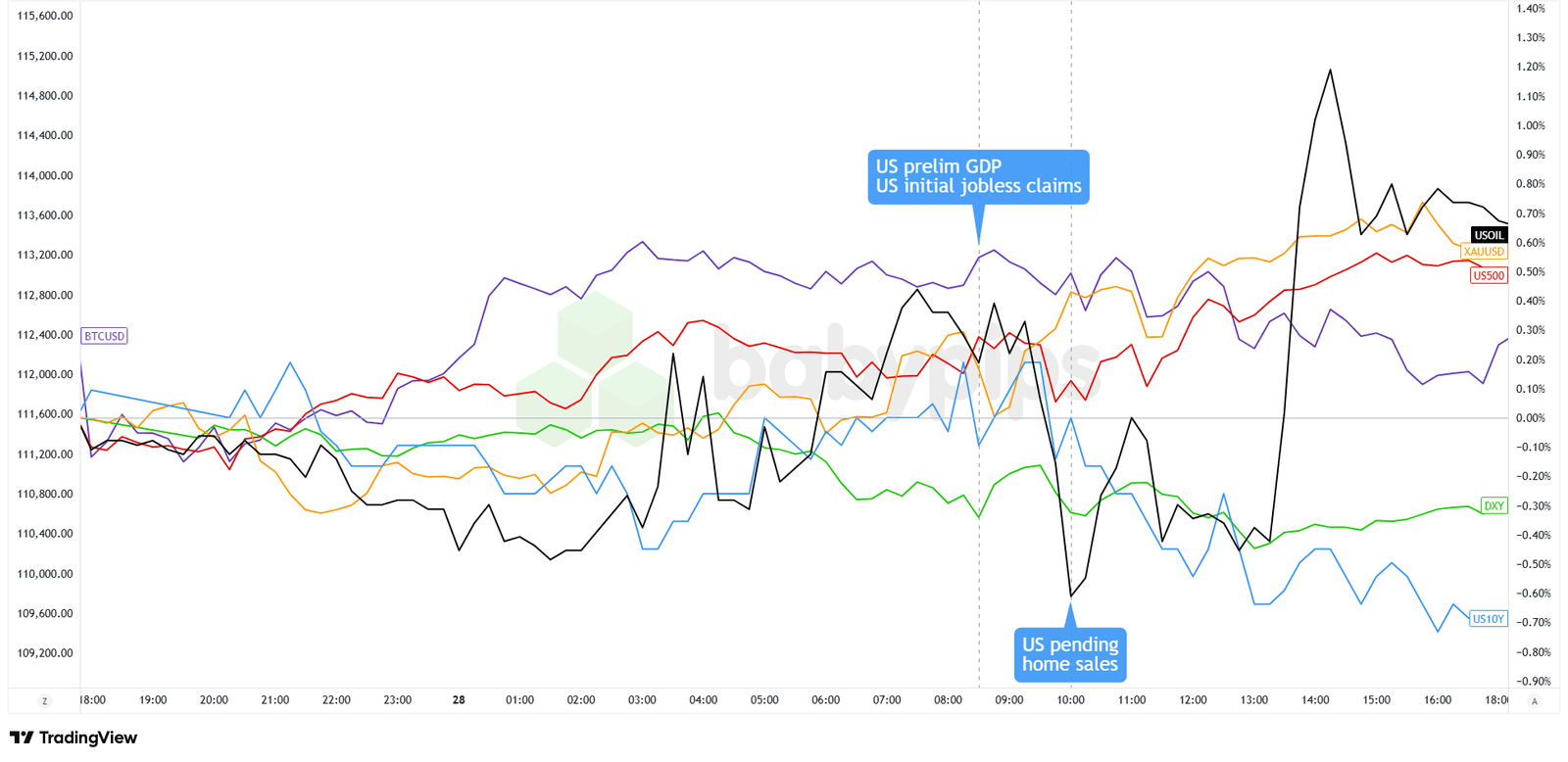

Gold advanced to $3,415, supported by Fed rate cut expectations and political pressure on the central bank following Trump’s attempt to fire Governor Lisa Cook. The 10-year Treasury yield fell to 4.21%, marking its third consecutive decline.

Meanwhile, WTI Crude oil gained 0.65% to $64.30 as Russia-Ukraine peace efforts stalled amid overnight Russian bombardments that killed 18 people, while the U.S. imposed penalty tariffs on India to discourage Russian oil purchases. Bitcoin rallied to $112,400, benefiting from broad dollar weakness as traders priced in an 87% probability of a September rate cut.

FX Market Behavior: U.S. Dollar vs. Majors:

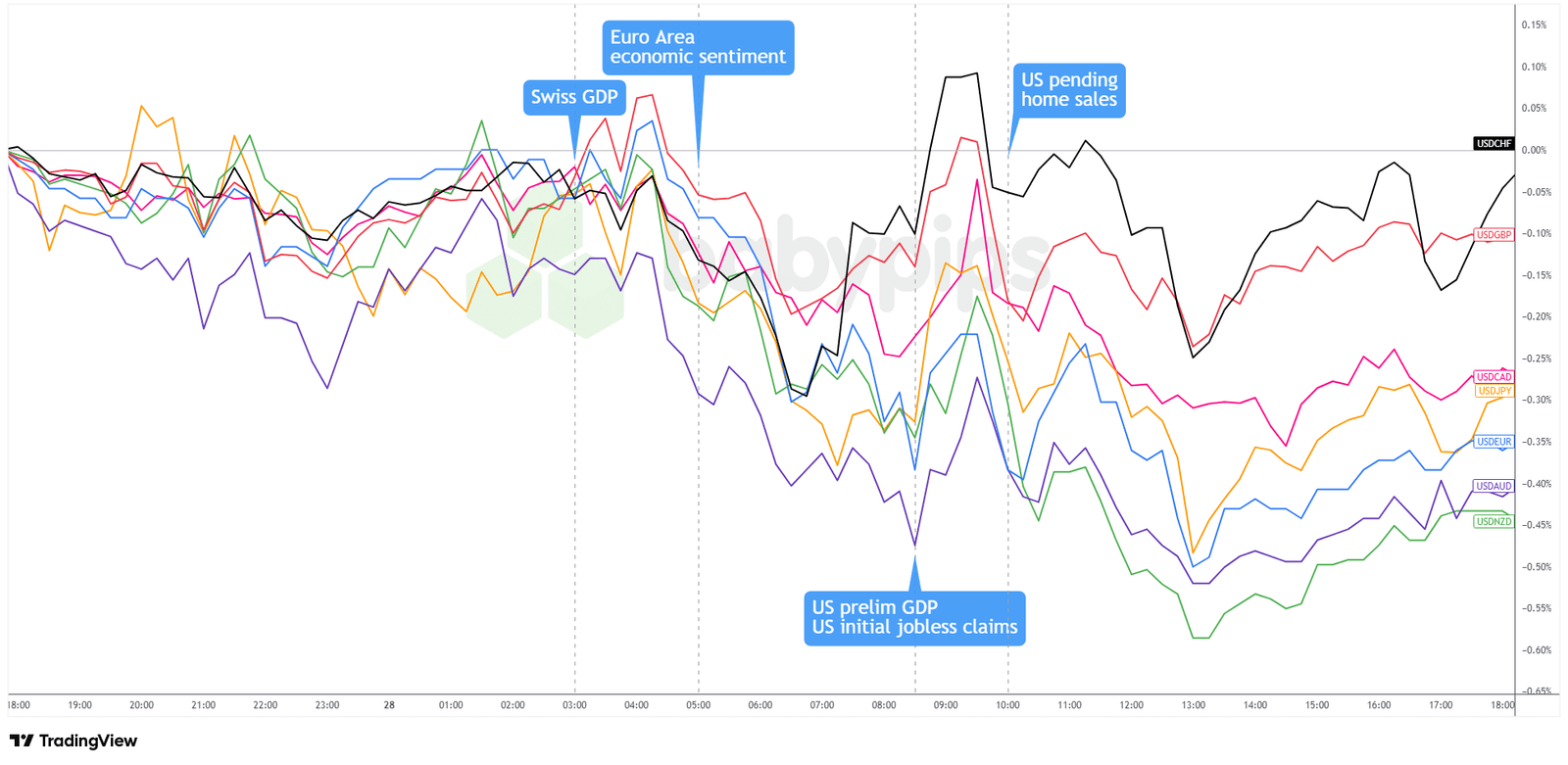

Overlay of USD vs. Majors Chart by TradingView

The dollar extended its decline Thursday, weakening against all major currencies as traders increasingly positioned for a September rate cut. The Greenback started the session on the back foot after NY Fed President Williams shared September’s meeting was “live,” reinforcing market expectations for monetary easing.

The dollar briefly pared losses during early European trading but quickly resumed its downward trajectory, likely as European traders positioned defensively ahead of Friday’s core PCE data.

A temporary reprieve came during the US session when stronger-than-expected GDP data showed the economy expanding at a 3.3% annualized pace, above the 3.1% estimate, while initial jobless claims fell to 229,000, better than the 230,000 forecast. However, the dollar’s bounce proved fleeting as the political drama surrounding Trump’s attempt to fire Fed Governor Lisa Cook continued to weigh on sentiment, with traders viewing the administration’s pressure as likely to produce a more dovish central bank.

The Greenback traded defensively through the London close and into the New York afternoon, ending lower across the board. Market participants remained focused on the Fed’s next move, with swap contracts pricing in an 87% probability of a quarter-point cut next month.

Upcoming Potential Catalysts on the Economic Calendar

- Germany retail sales for July at 6:00 am GMT

- Germany import price index for July at 6:00 am GMT

- France inflation rate prel for August at 6:45 am GMT

- France GDP growth rate final for Q2 2025 at 6:45 am GMT

- Germany unemployment change & rate for August at 7:55 am GMT

- Euro Area ECB consumer inflation expectations for July at 8:00 am GMT

- Euro Area ECB De Guindos speech at 9:00 am GMT

- Germany inflation rate prel for August at 12:00 pm GMT

- Canada GDP growth rate annualized for Q2 2025 at 12:30 pm GMT

-

U.S. core PCE price index for July at 12:30 pm GMT

- U.S. personal income & spending for July at 12:30 pm GMT

- U.S. wholesale inventories adv for July at 12:30 pm GMT

- U.S. goods trade balance adv for July at 12:30 pm GMT

- U.S. Chicago PMI for August at 1:45 pm GMT

- U.S. Michigan inflation expectations final for August at 2:00 pm GMT

- U.S. UoM consumer sentiment index for August at 2:00 pm GMT

- Canada budget balance for June at 3:00 pm GMT

Markets are heading into a data-heavy day that could cause increased volatility for both the euro and the dollar. The London session brings German retail sales, unemployment, and inflation figures alongside French GDP and inflation, likely steering euro sentiment ahead of ECB comments.

In the U.S., the spotlight is on the core PCE report – the Fed’s preferred inflation gauge – which could make or break September rate cut expectations. Personal income, spending, trade balance, and Chicago PMI follow, while consumer sentiment and Canada’s GDP and budget balance will keep traders busy into the afternoon.

As always, look out for global trade developments and geopolitical headlines that could influence overall market sentiment. Stay nimble and don’t forget to check out our Forex Correlation Calculator when taking any trades!