With no fresh catalysts, the major currencies danced to the tune of Fed expectations and market risk sentiment.

Meanwhile, other major assets kept grinding along as traders weighed mixed economic data, central bank speculations, and fresh geopolitical headlines.

Here’s how major asset classes performed in the latest trading sessions!

Headlines:

- BOC Gov. Macklem rules out review of 2% inflation target amid supply chain and tariff uncertainty

- Australia CPI for July 2025: 2.8% (2.0% forecast; 1.9% previous)

- AUD jumps as Australia’s July CPI dampened RBA easing hopes, but gains limited

- China industrial profits (YTD) for July: -1.7% y/y (-1.8% y/y forecast; -1.8% y/y previous)

- Russian army has reportedly crossed into Ukraine’s Dnipropetrovsk region

- Ukrainian drone attack sparks fire, evacuations in Russia’s Rostov region

- Germany GfK consumer confidence for September: -23.6 (-21.3 forecast; -21.5 previous)

- Swiss economic sentiment index for August: -53.8 (-1.0 forecast; 2.4 previous)

- EU reportedly seeking to fast track legislation by the end of the week to remove all tariffs on US industrial goods

- Trump’s 50% tariff on India kicks in as Modi urges self-reliance

- U.K. CBI distributive trades for August: -32.0 (-30.0 forecast; -34.0 previous)

- U.S. MBA 30-year mortgage rate for August 22, 2025: 6.69% (6.68% previous)

- U.S. EIA crude oil stocks change for August 22, 2025: -2.39M (-6.01M previous)

- Mexico to raise tariffs on imports from China after US push

- Fed’s Barkin forecasts modest rate adjustment, stops short of signaling support for September cut

- Fed’s Williams needs to see how data play out to consider September cut

Broad Market Price Action:

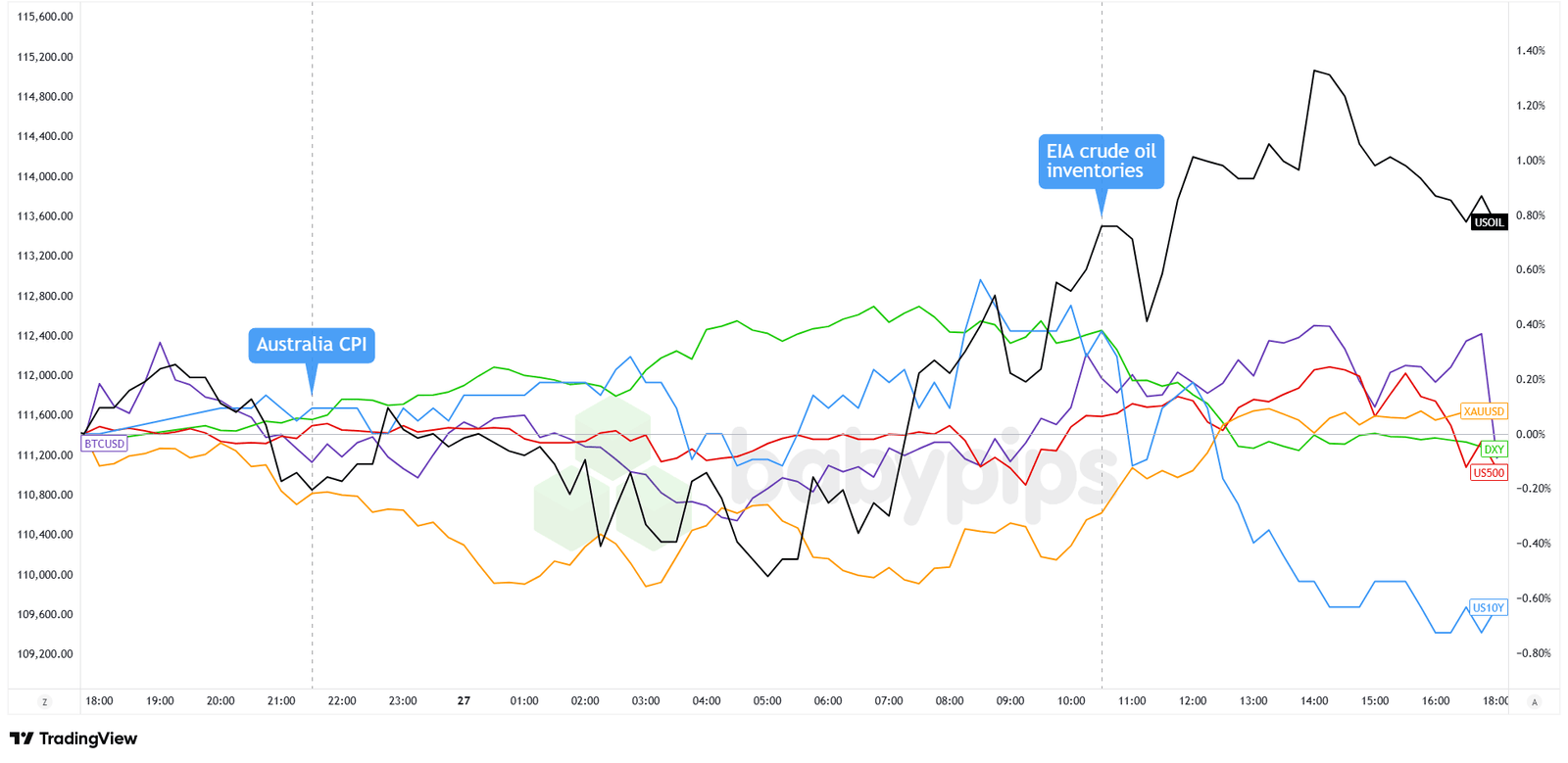

{kind=link}

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

With not a lot of fresh catalysts to chew on, markets continued to price in Fed independence concerns as well as mixed economic signals and geopolitical updates.

European equities finished mixed, with France’s CAC 40 gaining 0.44% amid relief that Prime Minister Bayrou’s government survived another day ahead of the September 8 confidence vote, while Germany’s DAX fell 0.44% after consumer confidence plunged to -23.6, far worse than expected. The S&P 500 notched its nineteenth record close of 2025, rising 0.24%, with energy stocks leading on oil strength while investors positioned ahead of Nvidia’s after-hours earnings.

Gold extended gains to $3,398 as traders sought haven assets amid unprecedented Fed politicization following Trump’s attempt to fire Governor Cook. The ten-year Treasury yield dipped to 4.238% from 4.274% as the curve steepened dramatically, reflecting market expectations of politically-influenced near-term rate cuts but rising long-term inflation risks.

WTI crude surged 1.42% to $64.15 after EIA data showed another substantial inventory draw of 2.392 million barrels, while Russia-Ukraine tensions and Trump’s tariff threats on India over Russian oil purchases heightened supply concerns. Bitcoin remained range-bound near $111,500, unable to make new weekly highs despite a slight risk-on sentiment.

FX Market Behavior: U.S. Dollar vs. Majors:

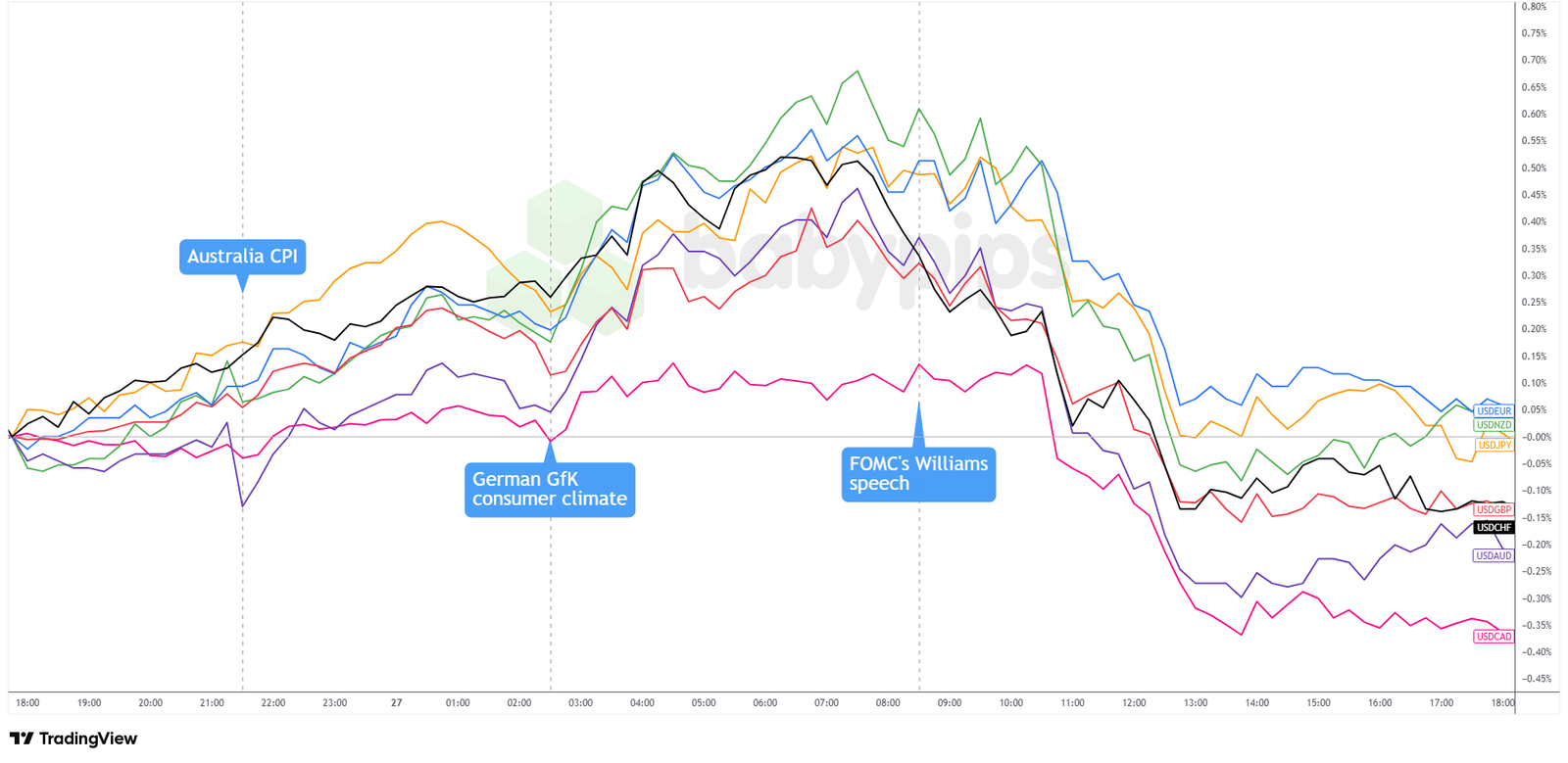

Overlay of USD vs. Majors Chart by TradingView

The dollar exhibited a volatile session Wednesday, initially strengthening in Asian and European trading as markets fully priced in two Fed rate cuts for 2025 while escalating Russia-Ukraine tensions drove safe-haven demand.

Australia’s July CPI surprised to the upside at 2.8% annually versus 2.3% expected, briefly boosting the Aussie before broader dollar strength resumed. The yen also weakened in Asia, with USD/JPY edging above 147.80 from below 147.30, despite confirmation that Japan’s chief trade negotiator Akazawa would return to Washington Thursday for investment talks. The Chinese yuan bucked the trend, strengthening to its highest level against the dollar since November despite weak industrial profits data showing a 1.5% year-over-year decline in July, marking a third consecutive monthly drop.

The Greenback’s momentum reversed around the early U.S. session as Fed independence concerns resurfaced following Trump’s attempt to fire Governor Cook; traders were likely pricing in expectations of more dovish policies under political pressure.

NY Fed President Williams provided measured commentary on CNBC, stating rates would likely fall at some point but emphasized policymakers need to see upcoming economic data before deciding on a September cut, adding that “every meeting is live” for potential changes.

The dollar ended the day mixed, managing small gains against EUR, NZD, and JPY but lower against relatively strong CHF, AUD, CAD, and GBP.

Upcoming Potential Catalysts on the Economic Calendar

- Swiss GDP growth rate for Q2 205 at 7:00 am GMT

- Euro Area consumer inflation expectations for August at 9:00 am GMT

- Euro Area consumer confidence for August at 9:00 am GMT

- Euro Area ECB monetary policy meeting accounts at 11:30 am GMT

- Canada current account for June 30 at 12:30 pm GMT

- U.S. initial jobless claims for August 23 at 12:30 pm GMT

- U.S. GDP growth rate 2nd est for Q2 2025 at 12:30 pm GMT

- U.S. pending home sales for July at 2:00 pm GMT

- U.S. Kansas Fed manufacturing index for August at 3:00 pm GMT

- U.S. Fed balance sheet for August 27 at 8:30 pm GMT

- New Zealand ANZ Roy Morgan consumer confidence for August at 10:00 pm GMT

- U.S. Fed Waller speech at 10:00 pm GMT

Traders are in for a busy day with today’s data releases! Stronger Swiss GDP or hawkish tones in the ECB minutes could give EUR and CHF a lift in Europe, but weak confidence data would likely cap gains.

In the U.S., soft jobless claims or GDP could cement September cut bets and weigh on USD, while a firmer read or a hawkish Waller speech risks snapping the dollar back higher.

As always, look out for global trade developments and geopolitical headlines that could influence overall market sentiment. Stay nimble and don’t forget to check out our Forex Correlation Calculator when taking any trades!